refresh cycles may be increasing operational risk for businesses in Africa")

Global Print Expo 2026")

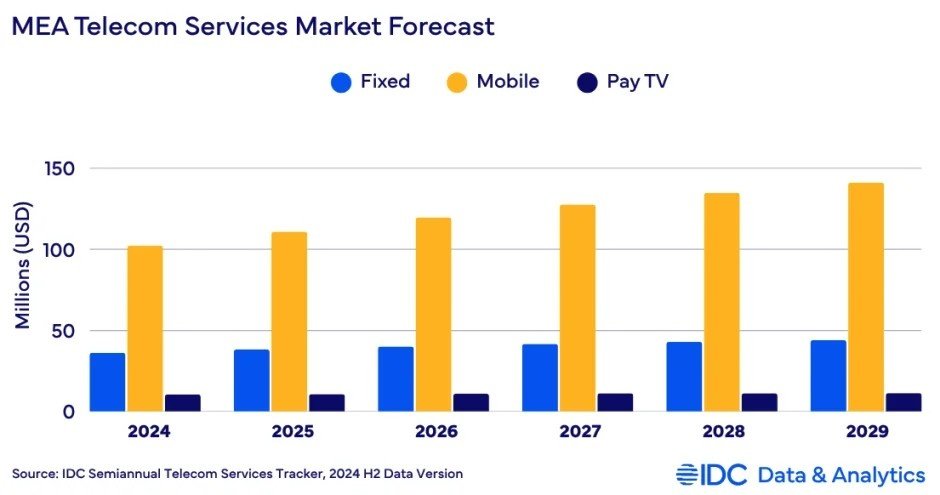

Communications services spending in the Middle East and Africa (MEA) reached $149 billion in 2024, growing 7.7 percent—well above the global average of 2.2 percent—according to IDC data. This robust momentum is expected to continue in 2025, with telecom and pay TV services forecast to rise 7.3 percent to $159.9 billion.

MEA led the global post-COVID telecom recovery in 2024, driven largely by infrastructure investments targeting expanded network coverage, especially in underserved African regions. Strong demand for mobile data persists despite tariff increases in high-inflation markets such as Türkiye, Egypt, Nigeria, Sudan, and Zimbabwe.

Consumer behavior is shifting from fixed voice toward mobile voice and data, supported by over-the-top (OTT) services, which dominate in markets where mobile phones serve as primary internet access points. While benefiting mobile revenues, this transition pressures legacy fixed-line services, noted IDC analyst Ivana Slaharova.

IDC’s latest forecast reflects some moderation due to tempered inflation and revised operator projections but remains positive overall.

Leading telecom operators in MEA are repositioning as technology companies (“techcos”), diversifying through digital transformation initiatives including AI, cloud-native platforms, edge computing, and accelerated 5G and fiber rollouts. While 5G is already active in Gulf countries, broader adoption across MEA is expected over five years, alongside growth in fiber and LEO satellite services.

Notable operator investments include:

- e& (formerly Etisalat) leading capital spending on 5G infrastructure, digital services, and international expansion.

- Saudi Arabia’s stc Group focusing on network modernization, 5G, and data centers aligned with Vision 2030.

- Ooredoo prioritizing digital innovation and cloud upgrades across Qatar, Oman, and Algeria.

- Zain Group advancing 5G in Kuwait and Saudi Arabia, with fintech and data monetization initiatives.

- MTN Group investing heavily in rural connectivity, 5G pilots, and fintech in South Africa and Nigeria.

- Vodacom expanding fiber and broadband services through partnerships and acquisitions.

- Orange enhancing mobile and fixed networks in North and West Africa, growing digital banking and enterprise solutions.

These operators increasingly collaborate with global tech and cloud providers to meet rising enterprise and digital demand.

However, risks remain from geopolitical tensions, trade disputes, and U.S.-imposed telecom equipment tariffs, which could elevate costs and delay infrastructure projects such as 5G and AI deployments. These challenges may indirectly affect spending by impacting broader economic conditions and consumer purchasing power, though current direct impacts on telecom revenues are limited.