Since traditional remittance providers typically require immediate payment, Send Now, Pay Later aims to address this critical pain point and provide vital service to customers who are new to the country and have a limited UK credit history.

LONDON, United Kingdom, October 9, 2025/ —

- International payments platform LemFi allows over 2 million immigrants to easily send money across the globe

- LemFi uses AI within its robust credit service to enable ‘send now, pay later’ remittance, so people can ensure their families are supported when they need it most

- New product will help streamline nearly £10 billion worth of payments

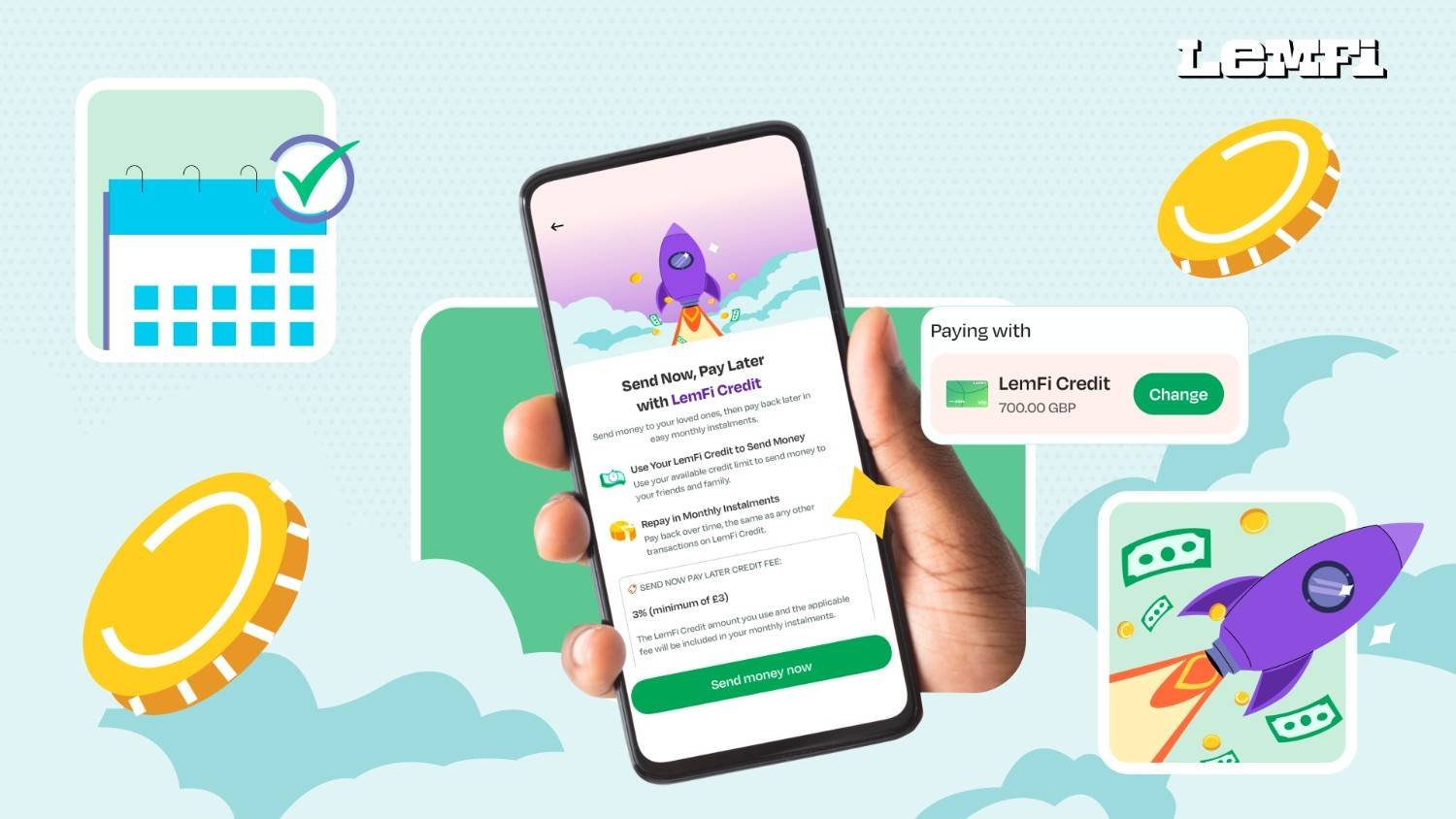

LemFi (https://LemFi.com), the leading AI-powered international payments platform dedicated to building financial products and services for immigrant communities, today announced the launch of Send Now, Pay Later (SNPL), a credit-powered remittance product that allows its UK customers to use their LemFi credit line to send money home to their families when they need it most.

For the millions of immigrants in the UK who send nearly £10 billion back home annually (https://apo-opa.co/4ohJsCl), there is often a timing mismatch between unexpected expenses and local earning cycles. This can force them to delay pivotal transfers home or turn to unregulated, expensive credit solutions. Since traditional remittance providers typically require immediate payment, Send Now, Pay Later aims to address this critical pain point and provide vital service to customers who are new to the country and have a limited UK credit history.

Powering SNPL is LemFi’s Ensemble AI model, which combines multiple data sources to inform credit decisions, including national credit bureaus, open banking data, and the company’s own remittance data, to help determine credit limits and repayment structures. This intelligent system also automatically adjusts depending on the individual customer’s journey and available data points, determining the required data points based on the customer’s circumstances and then offering risk-adjusted credit based on the available data.

Ridwan Olalere, co-founder and CEO of LemFi, said: “The rise of Buy Now, Pay Later means people across the world can buy products and stagger the payments depending on their cash flow. But this has never been possible before with remittance, despite it being such a core part of the immigrant financial experience. With Send Now, Pay Later, we’re integrating credit directly into the remittance experience, ensuring financial support is never delayed by cash flow timing. It’s also a testament to our commitment to building a full-stack, AI-enabled financial ecosystem that understands and serves the unique challenges faced by global citizens.”

How Send Now, Pay Later Works

To access SNPL, LemFi customers are onboarded to LemFi Credit, which gives users access to credit lines ranging from £300 to £1,000, depending on their credit profile and assessment, which is enabled by leveraging open banking technology to evaluate eligibility. This makes it accessible even to recent immigrants who often lack extensive UK credit histories and are excluded from traditional finance services. In addition, LemFi’s platform can recognise international credit histories and employs alternative credit assessment methods that look beyond traditional UK financial records. This allows users to start with smaller credit limits and build their UK credit profile over time while accessing essential financial services.

This is done through the company’s AI-driven decisioning engine that analyses a wide spectrum of data points, including open banking insights, bureau files, remittance history and patterns within LemFi, as well as international credit footprints. By training models across these diverse datasets, LemFi can predict affordability and repayment likelihood with greater accuracy than traditional scoring approaches while reducing bias that often excludes immigrants from mainstream credit, helping to solve the issue of “credit invisibility” through the application of artificial intelligence.

Once onboarded, customers can access their credit limit to send money to any of the 30+ LemFi-supported destination countries. When choosing the SNPL option, LemFi immediately processes the transfer to the recipient while creating a deferred payment obligation for the sender.

Bridging the Credit Divide

Currently, immigrants face significant and widespread issues when it comes to trying to access credit and banking services more broadly. Approximately five million individuals in the UK are considered “credit invisible”, with immigrants from emerging countries disproportionately affected. Research indicates (https://apo-opa.co/3VT1bUt) that nine in 10 immigrants report that accessing credit has become more difficult in recent years, while 13% of migrants are excluded from banking services compared to just 3% of the general UK population. This exclusion creates a cascade of financial challenges that extend beyond simple access to credit.

LemFi’s approach to credit assessment specifically addresses these challenges. As well, SNPL will tackle friction points around timing and bank transfers. Its real-time / same-day transfers reduce the time taken by traditional banks by a third and provide a means for its users to support their community despite their cash flow.

Global Expansion and Market Opportunities

Following the UK launch, LemFi plans to expand the SNPL service to its other markets in the United States, Canada, and Europe. It currently supports over 2 million customers, enabling them to send money to over 30 countries across Asia, Africa, Europe, and Latin America.

Since its founding, LemFi has supported over 2 million customers in the United States, the United Kingdom, Canada, and Europe. In January 2025, LemFi secured $53 million in Series B funding, bringing its total funding to over $86M. Investors include Highland Europe, LeftLane Capital, Endeavor Capital, and Y-Combinator.

For more information, visit https://LemFi.com.

Distributed by APO Group on behalf of LemFi.