to reveal and support innovative entrepreneurship and impact projects")

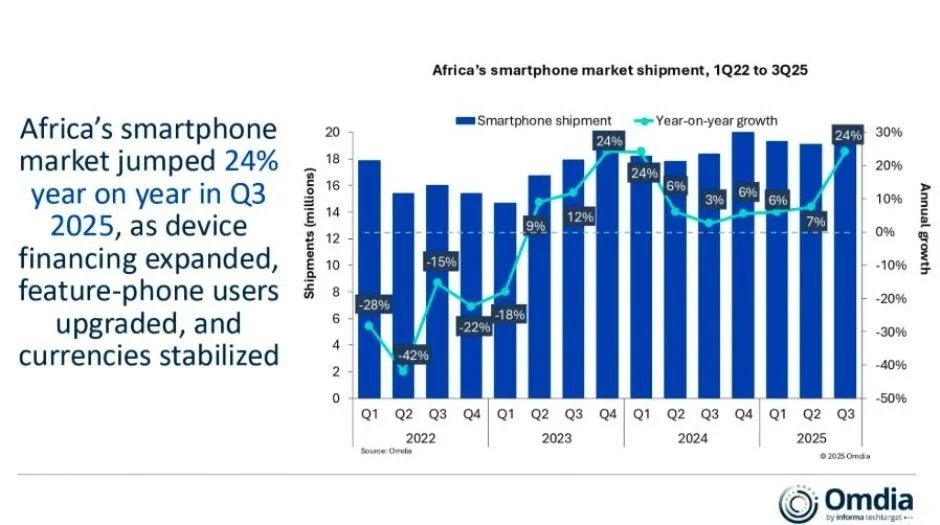

Africa’s smartphone market staged a powerful comeback in the third quarter of 2025, with shipments rising 24 percent year on year to reach 22.8 million units, according to new data from Omdia. The recovery outpaced global trends and ended a five-quarter period of decline across the continent.

Analysts attribute the rebound to stabilising currencies, expanding device-financing options, and stronger retail activity across major African markets. Transsion led the market with 11.6 million units shipped, followed by Samsung (3.4 million), Xiaomi (2.9 million), Oppo (1 million), Honor (0.9 million), and other brands accounting for 3.1 million units.

Most markets in North and Sub-Saharan Africa recorded double-digit growth, with only Algeria posting modest expansion at 4 percent. Nigeria and Egypt each captured 14 percent of total shipments but for different reasons: Nigeria saw a 29 percent jump as vendors boosted imports and refreshed sub-USD 150 models, while Egypt grew 19 percent driven by strong mid-range demand between USD 150 and USD 250.

South Africa was the standout performer with 31 percent growth, powered by prepaid demand and strong promotions from major retailers such as Pepkor and Ackerman’s. The removal of the 9 percent ad valorem tax further boosted sales. Kenya grew 17 percent as device-financing programmes expanded, making upgraded entry-level smartphones more accessible.

Omdia’s data shows an unusual dual surge across price segments: sub-USD 100 devices rose 57 percent, while the premium above-USD 500 tier grew 52 percent. Transsion strengthened its dominance in the entry segment with refreshed TECNO, Infinix, and itel models, while Samsung led the premium category with strong Galaxy S24 and S24 FE traction across South Africa, Senegal, and Algeria.

Xiaomi continued expanding its African footprint—opening its first owned store in Morocco and preparing entry into more than 15 additional markets—while Oppo increased its North African presence and Honor maintained momentum in South Africa through competitive value-focused models.

Despite the strong Q3 results, Omdia forecasts a 6 percent market decline in 2026 due to supply-side pressures, including rising component costs, memory constraints, higher shipping expenses, and currency headwinds. These factors are expected to raise average selling prices, particularly in the USD 80–150 range, posing affordability challenges. Vendors that invest in financing partnerships, efficient channels, and localized operations will be best positioned to maintain upgrade cycles in the tougher market environment.